Double-declining balance depreciation method: Definition, benefits, and accounting basics

Learn everything you need to know about the double-declining balance method: what it is, how to calculate it, and the benefits of more accurate asset valuation.

From the moment you purchase property, plant, and equipment (PP&E) assets, their value starts to decline. Your accounting strategy needs to reflect this depreciation so you can align expenses with revenue and pay the right taxes to stay in line with financial reporting standards.

While straight-line depreciation rates offer more stable expense reporting, the double-declining balance method takes a more detailed—and often realistic—view. It accommodates fixed assets like machinery, vehicles, or technology that depreciate rapidly at first, before slowing as time goes on.

This guide will break down everything you need to know about the double-declining balance method: what it is, how to calculate it, and the benefits of more accurate asset valuation.

What is the double-declining balance method?

The double-declining balance (DDB) method is a widely used asset depreciation method. It’s a form of accelerated depreciation that allows businesses to allocate a higher portion of an asset's cost as an expense in the earlier years of its useful life.

This method assumes that assets tend to lose their value more rapidly in their initial years of operation and gradually slow down in depreciation over time, which accounting teams track with a depreciation journal entry.

DDB is most suitable for assets that exhibit a faster decline in their value early in their useful lives, such as:

- Technology and equipment: Assets like computers, smartphones, and specialized machinery often rapidly decrease in value as newer, more advanced versions are developed. Double-declining balance depreciation may more accurately reflect the rate of equipment depreciation.

- Vehicles: Automobiles and other vehicles typically experience significant depreciation in their first few years due to wear and tear, making DDB suitable for reflecting this decline.

- Software: Computer software can become obsolete relatively fast as companies introduce new versions or technological advancements. Using DDB matches the declining value of software assets.

- Leasehold improvements: Improvements made to rental properties, such as tenant fit-outs, can depreciate rapidly, and the DDB method is useful for capturing this decline.

- Certain types of machinery: Some specialized machinery may have a high rate of wear and tear, resulting in faster depreciation. The DDB method can accurately reflect this pattern.

- Short-lived assets: Assets with relatively short expected useful lives, such as certain types of tools or equipment, are good candidates for the DDB method.

How the double-declining balance method works

Double-declining balance depreciation applies a fixed rate to an asset's decreasing book value each year. This rate is double the straight-line depreciation rate. By doubling the depreciation rate, the method accelerates the recognition of depreciation expenses, resulting in lower book values for assets on the balance sheet in the initial years.

Double-declining balance method formula

The double-declining balance method uses the following formula to calculate annual depreciation:

Depreciation expense = (2 x straight-line depreciation rate) x book value at the beginning of the year

Where:

- The straight-line depreciation rate is 1 divided by the amount of years in the asset’s useful life.

- Book value is the asset’s value at the start of each year, after subtracting accumulated depreciation.

This formula accelerates depreciation by applying a higher expense in the earlier years of the asset’s useful life. Unlike straight-line depreciation, the DDB method doesn’t consider salvage value in calculations until the final year, when the book value approaches the salvage value.

Double-declining balance method vs. straight-line depreciation

DDB and straight-line depreciation both allocate the cost of an asset over its useful life, but they differ significantly in their approach:

- Expense allocation

- The straight-line method spreads the depreciation expense evenly over the asset’s useful life. This results in consistent annual depreciation amounts, making it simple and predictable.

- The double-declining balance method, on the other hand, accelerates depreciation by allocating a higher expense in earlier years and decreasing amounts over time.

- Application

- Straight-line depreciation is ideal for assets that lose value consistently, such as buildings or long-lasting office furniture.

- The double-declining balance method suits assets that depreciate rapidly, like technology or vehicles, providing a more realistic reflection of their usage and wear.

- Impact on financial statements

- Straight-line depreciation provides stable expense reporting, making it easier for long-term financial planning.

- DDB affects early financial statements more significantly, as it reduces book value and taxable income faster, potentially leading to short-term tax benefits.

To better understand the financial impact of these methods, let’s look at a hypothetical example:

Imagine a company purchases a machine for $50,000 with an estimated useful life of 5 years and no salvage value.

With straight-line depreciation, the machine’s cost is evenly spread across its useful life, resulting in an annual depreciation expense of:

$50,000 / 5 = $10,000

Each year, the company deducts $10,000, providing consistent expense reporting and making it easy to forecast future profits.

Using the double-declining balance depreciation method, the first year’s depreciation expense is:

(2 x 0.2) x $50,000 = $20,000

The book value at the end of year one drops to $30,000, and the depreciation expense decreases in subsequent years.

This difference shows how the DDB method significantly reduces taxable income upfront, which can benefit cash flow. In contrast, the straight-line method smooths out expenses over time, which is useful for businesses that prioritize financial predictability.

Choosing between the two depends on the nature of the asset and the business’s financial strategy. Both methods comply with the Generally Accepted Accounting Principles (GAAP) and offer different advantages depending on your financial goals and the asset type.

How to calculate depreciation using the double-declining balance method

Calculating depreciation using the DDB method requires consistent application of the formula consistently throughout the asset’s useful life. Here’s a step-by-step guide to calculating depreciation:

1. Determine the straight-line depreciation rate

Divide one by the asset’s useful life. For example, if the asset has a useful life of five years, the straight-line depreciation rate is:

1 / 5 = 0.2 (20% per year)

2. Double the straight-line rate

To calculate the DDB rate, multiply the straight-line rate by two:

0.2 x 2 = 0.4 (40% per year)

3. Apply the DDB formula

Use the formula:

Depreciation expense = (2 x straight-line rate) x book value at the beginning of the year

For an asset with an initial book value of $50,000, the first year’s depreciation would be:

0.4 x $50,000 = $20,0000

4. Update the book value annually

Subtract the depreciation expense from the book value to calculate the new book value for the next year:

$50,000 − $20,000 = $30,000

Repeat the process for each subsequent year until the book value approaches the salvage value.

5. Adjust for salvage value in the final year

The DDB method doesn’t consider salvage value in annual calculations, but it does make sure the asset’s book value doesn’t drop below its salvage value. If necessary, adjust the depreciation expense in the final year to match the salvage value.

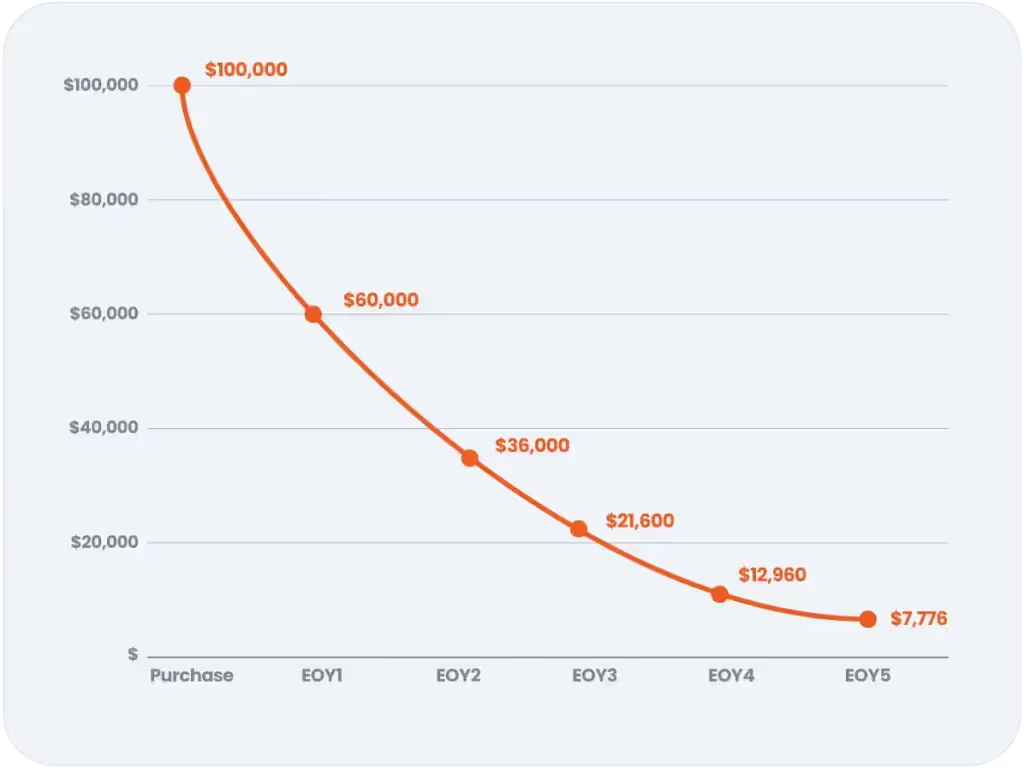

Double-declining balance depreciation example

By correctly calculating the depreciation each year, accountants can accurately reflect the diminishing value of an asset on the company's financial statements.

Imagine a company purchases machinery for $100,000 with an estimated useful life of 5 years and no salvage value. Here's how you would apply the double-declining balance method:

Year 1:

- Straight-line depreciation = ($100,000 - $0) / 5 = $20,000

- Double-declining balance depreciation = (⅕)*2*$100,000 = $40,000

- Book value at year start = $100,000

- Book value at year-end = $100,000 - $40,000 = $60,000

Year 2:

- Double-declining balance depreciation = (⅕)*2*$60,000 = $24,000

- Book value at year start = $60,000

- Book value at year-end = $60,000 - $24,000 = $36,000

Benefits of the double-declining balance method

The double-declining balance method has many benefits for the right kinds of fixed assets, including:

- Accelerated depreciation: The double-declining balance method allows for higher depreciation expenses in the earlier years of an asset's life, which can provide a more accurate representation of its decreasing value over time.

- Matching expenses: It helps in matching depreciation expenses with the higher revenue generated by an asset in its earlier years, which may result in more accurate income statements.

- Tax benefits: Accelerated depreciation may lead to lower taxable income in the short term, resulting in reduced income tax liabilities.

- Reflects realistic wear and tear: This method is especially suitable for assets that experience significant wear and tear in their initial years, providing a more realistic representation of their decreasing value.

- Budgeting and planning: It aids in better financial planning and budgeting by accurately reflecting the asset's declining value over its useful life.

Downsides to the double-declining balance method

While the double-declining balance method has its advantages, it also has some drawbacks:

- Lower book values: Assets can have lower book values on the balance sheet in the initial years, affecting financial ratios and the perception of a company's financial health.

- Complexity: Calculating depreciation using this method can be more complex than using the straight-line method, which may require specialized accounting knowledge (or accounting solutions that automate the process).

Learn more about the double-declining balance method

Find answers to the most common questions about double-declining balance depreciation.

What is depreciation?

Depreciation is the accounting process of spreading the cost of a tangible asset over its useful life. It shows how an asset’s value decreases over time due to wear and tear, usage, or obsolescence. Depreciation allows businesses to match the expense of using an asset with the revenue it helps generate, which provides more accurate financial reporting.

Is the double-declining balance method allowed under Generally Accepted Accounting Principles (GAAP)?

Yes, the method is an acceptable depreciation method under GAAP. It's important to ensure that its application complies with the specific guidelines and requirements of GAAP.

What happens if an asset's book value falls below its salvage value using the double-declining balance method?

If an asset's book value falls below its salvage value during the depreciation process, adjust the depreciation expense in that year to ensure it doesn’t go below the salvage value. This adjustment ensures that the asset's book value never falls below its expected salvage value.

Are there limitations to using the double-declining balance method for financial reporting?

While the method is a valuable tool for reflecting the depreciation of certain assets accurately, it may not be suitable for all situations. For financial reporting, consider the appropriateness of this method for your specific circumstances and adhere to the relevant accounting standards and regulations.

What is the relationship between accumulated depreciation and the double-declining balance method?

Accumulated depreciation is the cumulative depreciation expense recognized as an asset over its lifetime. Under the double-declining balance method, accumulated depreciation accumulates more rapidly in the early years of an asset's life, reflecting accelerated depreciation.

How do I account for changes in an asset's useful life or salvage value when using the double-declining balance method?

If there are changes in an asset's useful life or salvage value, adjustments must be made to the depreciation calculation. These changes should be accounted for in the year they occur, and the depreciation expense should be adjusted accordingly.

Streamline depreciation calculations with accounting automation software

The double-declining balance method aligns asset depreciation with revenue generation, providing significant tax benefits and a realistic reflection of asset value. However, manually calculating depreciation for multiple assets can be time-consuming and error-prone, especially for businesses managing complex asset portfolios.

Netgain’s accounting automation solutions can transform your financial processes. Founded by Big 4 accountants, Netgain creates solutions for accountants’ biggest challenges. Our fixed asset management solutions help automate depreciation calculations, keep you compliant with GAAP, and give you real-time insights and reporting to save time and maintain accuracy.

So whether you need to monitor the depreciation of machinery, vehicles, tech, or all of the above, Netgain will help you take control of your asset management.

Learn more about Netgain’s fixed asset management solutions.